Cornucopia rock: forecast for the development of the Russian shoe market. Estimation of footwear market volume.

The crisis is the time to stop. To understand where, at what point in development we are, what is happening and how the situation will develop further. The Russian shoe market was analyzed by the leading consultant of Fashion Consulting Group Galina Kravchenko.

An objective assessment of the volume of the shoe market is difficult due to the lack of a reliable statistical base, as well as the actual presence on the market of unaccounted production and gray imports. At the same time, the reliability of existing announced data on market size is doubtful. Estimated shoe market volume in the media

| The minimum value | Maximum value | |

|---|---|---|

| current market size estimate, $ mln | 16 500 | 23 000 |

| current market volume estimate, mln pairs | 416, 6 | 635, 1 |

| the entire population of Russia, million people | 142 | 142 |

| average consumption (calculation), in pairs | 2,93 | 4,47 |

| average price (calculation), rub. for a couple | 976 | 893 |

Based on these data, the average consumption should be from 3 to 4,5 pairs per person, which is close to the European value. But that is unlikely, since the standard of living in Russia is much lower than in Europe. The estimated price corresponding to these numbers ranges from 976 to 893 rubles. These very low prices can only correspond to the prices of the spring-summer season, since the average price of shoes for the autumn-winter season is from 2000 to 3000 rubles. At the same time, the climatic features of Russia require the mandatory consumption of the most expensive winter shoes, as well as the purchase of shoes made from natural materials. Consequently, the average price of shoe consumption should be higher.

Methodology for calculating market volume

A more objective picture can be obtained on the basis of average consumption, as well as the structure of retail sales in Russia.

Market volume calculation based on average consumption

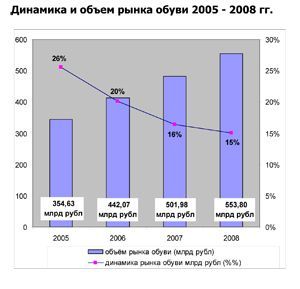

The population of Russia in 2008 amounted to 142 million people. According to experts, the average consumption in Russia is 2,6 pairs per year per person. Given the regional specifics, price ranges and seasonal types of shoes, the average price is 1500 rubles. Based on these data, the footwear market in 2008 is 369,2 million pairs and 553,8 billion rubles. ($ 22,4 billion).

The potential market volume can be considered 497 million pairs, which corresponds to the pre-perestroika level of consumption of 3,5 pairs per person. Thus, the market saturation in 2008 year is 74%, and the growth potential is 26%.

Calculation of the volume of the shoe market based on retail sales

According to Rosstat, retail sales in 2008 amounted to 13 853,2 billion rubles. At the same time, shoes, clothes and fabrics accounted for 13%, or 1800,9 billion rubles. The share of sales of fabrics is 0,03%. The clothing market is 1247,6 billion rubles. (as estimated by FCG). Accordingly, shoes account for 549,14 billion rubles. ($ 22,278 billion).

A comparison of these two estimates gives an error of less than 1% (0,83%), which allows us to talk about the objectivity of the calculations. Thus, the volume of the shoe market in Russia is 553,8 billion rubles.

Shoe market dynamics from 2005 to 2008

Despite the steady growth of the market, a decrease in its growth rates from 2005 to 2008. obviously. This indicates a gradual saturation. That is, even in the absence of a crisis, growth rates would continue to decline in the future.

Import of shoes and the structure of commodity circulation in the retail market by manufacturing countries

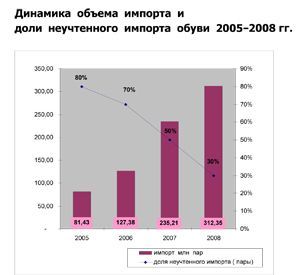

Official imports to Russia are growing annually: if in 2005, it amounted to 81,43 million pairs, then in 2008, it increased to 312,35 million pairs. At the same time, a reduction in unaccounted import from 80% in 2005 to 30% in 2008 is obvious. It is obvious that the reduced customs duties in the 2006 year led not only to an increase in the volume of imports of shoes in general, but also to a reduction in unofficial import of shoes into the country.

Structure of imports by countries in 2008 year (in value terms)

| The minimum value | Maximum value | |

|---|---|---|

| current market size estimate, $ mln | 16 500 | 23 000 |

| current market volume estimate, mln pairs | 416, 6 | 635, 1 |

| the entire population of Russia, million people | 142 | 142 |

| average consumption (calculation), in pairs | 2,93 | 4,47 |

| average price (calculation), rub. for a couple | 976 | 893 |

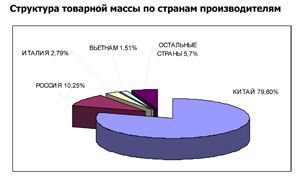

It is interesting to consider the structure of the commodity mass, taking into account Russian production (the share of Russian products in the market is about 10%), export operations, as well as consumption.

Production in Russia

Footwear production in Russia in 2008 increased by 2,5% and amounted to 52,05 million pairs (in 2007, 50,8 million pairs were produced). Men's shoes traditionally occupy the first place in the structure of production - 45% of the total output according to the results of 2007 of the year. This is partly due to the fact that one of the main customers for the shoe industry is government agencies. In second place in terms of output - women's shoes, in third - children's.

Domestic footwear has a strong competitive position in the segments of children's and special footwear, as well as in economy-class winter footwear. However, the breadth of the assortment range of Russian products is limited, so domestic production is able to produce only 5% of the consumed assortment.

The three leaders over the past few years have been pleased with their stability: Bris-Bosphorus, Ralph Ringer and Unichel.

A special place in the footwear industry is occupied by the shoe cluster in the Rostov Region. According to the calculations of the market players themselves, up to 300 shoe factories are operating in Rostov, of which about 100 are more noticeable. According to the Don Ministry of Industry, there are about 70 officially registered shoe enterprises in the region. The numbers vary, but one thing is certain: no region has so many small shoe manufacturers. The share of the Rostov region, according to some estimates, accounts for 25% of all domestic footwear products. Don shoe makers own the brands Walrus, Nine Lines, River Style, Yuros, Sasha, Santori, Oldie Don, Enrico, Main Line, Alex, Ascetic, Don Diamond.

Experts noted that each year there was a decrease in the number of domestic shoe manufacturing companies by 10 – 15%. However, in a situation of growing exchange rates, Russian producers are in a better position than importers. Thus, in February of 2009, Unichel CJSC increased production by 1,4%, and Magnitogorsk shoe factory plans to increase production in 2009 to 300 thousand pairs.

However, despite the potential possibility of increasing demand, experts have some doubts about the possibility of Russian production tripling output within two years if import customs duties are increased.

Recall that tripling of production volumes was mentioned in an open letter from Russian shoe manufacturers to the Prime Minister of the Russian Federation.

This means that by 2012, the share of Russian shoes in retail should be 31% (provided that the market does not grow). For such a short period of time, companies will not be physically able to find the required number of qualified personnel. Moreover, over the past five years, jobs have not increased, but been reduced.

Another pressing problem is that Russian manufacturers lack a wide range of products. And the expansion of the product range requires technical re-equipment. And it is unlikely that this problem will be solved in the near future, because the manufacturers themselves emphasize that everything rests on the absence of equipment manufacturers.

These are purely production factors that make the jump in production doubtful.

There are difficulties in the shoe industry with raw materials, and with components for production. The order of imported components (and their share in is about 70%) increases the cost of production, that is, the market factor is also included - price competitiveness.

Thus, an increase in customs duties on imported products will make it even more expensive for the final consumer, but this does not mean that Russian-made shoes will become more attractive to the buyer. And since imported products today amount to 90% of shoes consumed, it is obvious that the increase in duties will place an additional burden on the shoulders of the retail buyer.

Volume and segment dynamics

The key parameters for segmenting the shoe market are the price of shoes and gender and age characteristics of customers.

Price segments of the shoe market

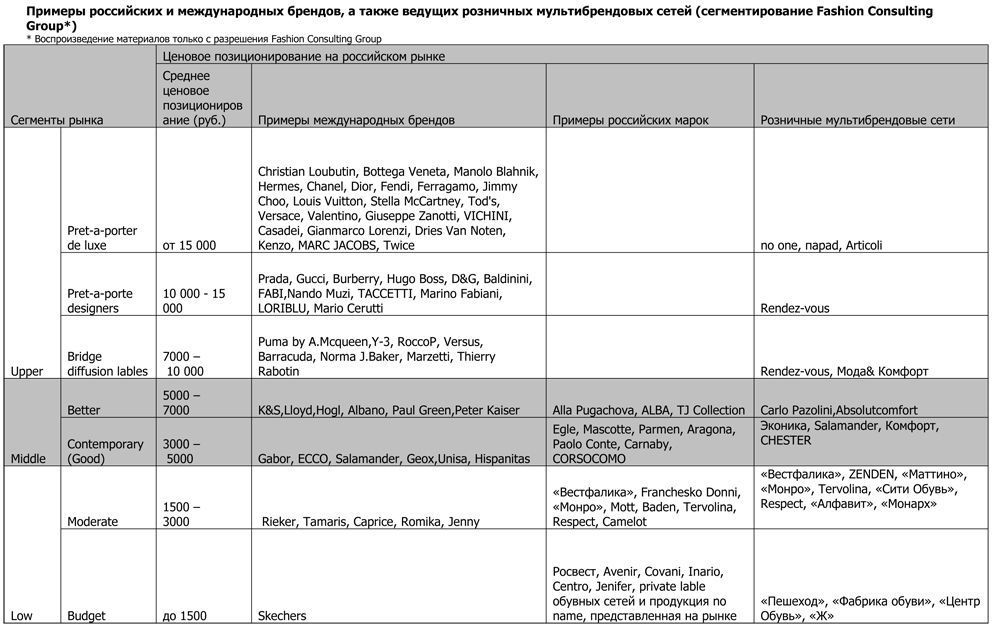

According to the price segmentation developed by Fashion Consulting Group, three main segments are distinguished in the footwear market: Low - the lower price segment, Middle - the middle price segment, Upper - the upper price segment.

The structure of the price segments of the shoe market

| The minimum value | Maximum value | |

|---|---|---|

| current market size estimate, $ mln | 16 500 | 23 000 |

| current market volume estimate, mln pairs | 416, 6 | 635, 1 |

| the entire population of Russia, million people | 142 | 142 |

| average consumption (calculation), in pairs | 2,93 | 4,47 |

| average price (calculation), rub. for a couple | 976 | 893 |

The most significant Low segment (lower price segment) occupies 50% of the market. It, in turn, is divided into two levels: Budget - the average price of women's shoes up to 1500 rubles .; Moderate - price range from 1500 to 3000 rub. for a pair of women's shoes. It is in the Moderate segment (40%) that the bulk of Russian shoe brands are represented: Westfalika, Franchesko Donni, Monroe, Mott, Baden, Tervolina, Respect, Ralf Ringer. There are also German brands: Rieker, Tamaris, Caprice. Budget footwear is presented mainly in uncivilized retail - in open markets and in discount stores Pedestrian, Shoe Factory, TsentrObuv, Zh. Low price involves the use of artificial or pressed leather for upper shoes, synthetic materials and textiles.

The Moderate segment is the most dynamic, as customers who previously preferred shoe markets and have shifted from the Budget segment have moved here. This confirms the active development of multi-brand retail chains: Westfalika, ZENDEN, Monroe, Tervolina, City Shoes, Respect, Ekolas, Easy Step.

The most promising is the lower part of the mid-price segment Middle - Contemporary (Good), shoes in the price range from 3000 rubles. to 5000 rub., which occupies 25% of the shoe market. The increase in the well-being of the population in recent years has led to an increase in the demand for quality and design. It is the combination of these characteristics with the optimal price that distinguishes the assortment of brands of this price niche. This segment includes both Russian brands, for example, Egle, Mascotte, Parmen, Aragona, Paolo Conte, Carnaby, CORSOCOMO, as well as foreign brands - leaders of the Russian market: Salamander, ECCO, Geox. Retail multi-brand formats of this segment are distinguished by a well-designed and recognizable corporate identity.

The most expensive Russian shoe brands are presented in the upper part of the Middle-Better segment (5000 - 7000 rubles): Alla Pugachova, ALBA, TJ Collection. Particularly noteworthy are the European brands popular in Russia positioned in this segment: K&S, Lloyd, Hogl.

In the upper price segment Upper are trendsetters: Christian Loubutin, Bottega Veneta, Manolo Blahnik, Jimmy Choo, Louis Vuitton, Tod's, Giuseppe Zanotti, VICINI, Casadei. The main share of this segment belongs to Italian brands, which quite logically reflects the world leadership of Italian footwear in this segment. This segment is characterized by a boutique format of trade, but there are also multi-brand networks: no one, Parad, Articoli, Rendez-vous, Fashion & Comfort.

Segmentation of the shoe market by age and sex characteristics of the consumer

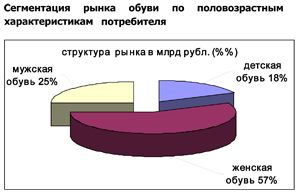

The share of women's shoes in the total market in monetary terms is 57%, men's - 25% and children's - 18%. Moreover, due to the difference in the average price for a couple, the market structure in physical terms is different: women's shoes - 53%, men's - 20%, children's 27%.

According to statistics, about 28,5 million children live in Russia. With an average consumption of 3,5 pairs of shoes per child per year, the market volume is 99,75 million pairs. For women, shoes lead by the frequency of purchases in the Spring-Summer season (39%). In the autumn-winter season, besides shoes (21%), ankle boots (27%) and ankle boots (25%) are in great demand. Among men's shoes, the undisputed leader in the spring-summer season is low shoes (40%), in the season "Autumn-Winter" shoes (57%) are in great demand.

Characteristics of distribution channels

The specifics of the Russian market is a mixture of wholesale and retail distribution channels in the sales of one company. So, historically large retail chains have appeared in companies engaged in wholesale sales: TsentrObuv, Westfalika, Monarch, Tervolina, Monroe, Unichel. Recently, there has been a tendency to transfer wholesale sales to the franchise sales system. This is typical primarily for networks of the mid-price segment Middle: Econika, Mascotte, Carlo Pazolini. Distributors of ECCO and Geox trademarks develop their own and franchised network. Franchising network companies: ALBA, Egle and Paolo Conte are moving ordinary wholesale customers to their own more affordable brands. Customers who do not work in the Paolo Conte corporate format are transferred to the new P.Cont brand. This allows you to work with the entire customer base, without abandoning smaller customers, and at the same time maintain a high image of the Paolo Conte brand. Accordingly, the company selling Egle shoes has a cheaper Fugo line, the company selling TM ALBA - SVETSKI.

“TsentrObuv”, “Westfalika”, “Monarch”, Tervolina, Zenden provide sales both by franchising and wholesale.

Thus, Russian companies, which in their pure form are engaged in only one type of activity, are rather isolated examples. Most of the wholesale companies are German and Italian manufacturers: Rieker, Ara, Gabor, Baldinini, FABI, Nando Muzi, TACCETTI, Marino Fabiani, K&C, Lloyd, Paul Green, Peter Kaiser, Marco Tozzi, Caprice, Tamaris, Jana, etc. Moreover, some of them open their own representative offices in Russia, some take orders only at exhibitions.

Russian manufacturers also have their own retail: Unichel and Antelope.

Exclusively retail trade in footwear is carried out by companies that own multi-brand networks: Mattino, Zh, Rendez-vous, Fashion & Comfort, no one, Parad.

Retail Formats

There are two distinct types of retail sales on the Russian shoe market: civilized and uncivilized retail. “Uncivilized format” refers to retail sales that take place in clothing markets, exit fairs, off-board trucks and folding temporary shelves. The dynamic development of civilized forms of trade became possible with the advent of large shopping centers, malls and hyper malls.

The formats of civilized retail trade in shoes in Russia can be classified on the following grounds:

1. By type of business:

- single stores (Independent store);

-network stores (own or franchised) (chain);

2. Assortment formation:

- multi-brand stores;

- monobrand stores;

3. By breadth of assortment - by the number of product categories:

- standard department store (department stores-full-line);

- specialized department store (department stores limited-line);

- a specialized store (specialty stores).

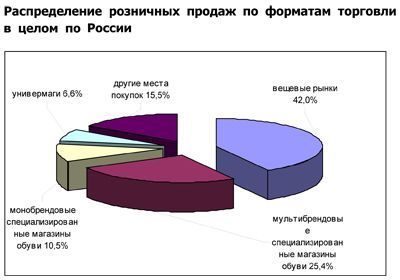

According to expert estimates, about 40% of shoes are bought on the market, 36% - in specialized stores, the rest - in department stores and other retail formats. Therefore, the development vector of shoe retail in recent years has not changed - a reduction in the share of customers who prefer clothing markets.

Distribution of retail sales by trade formats in Russia as a whole

According to analysts, in some regions the market share as the preferred place of purchase exceeds 50%. It is noteworthy that in Moscow and St. Petersburg the share of specialized stores now exceeds the market share. A significant trend in recent years has been the emergence of large shoe centers focused on consumers with low and medium incomes.

Experts rate the level of competition in the domestic retail footwear market as average. No company has even reached 1% of the market. In Russia, it is very difficult to achieve a larger share due to geographical, climatic and mental features, as well as due to the lack of necessary skills and competencies for shoe companies for effective network management.

The largest shoe chains include:

- TsentrObuv (309 stores)

- Ecco (185 stores)

- Unichel (160 stores)

- "Monarch" (159 stores)

- Tervolina (150 stores)

- Econika (107 stores)

- Monroe (90 stores)

- Westfalika (88 stores)

- Ralph Ringer (69 stores).

In recent years, shoe retail has grown very dynamically: the number of stores within the chains has increased one and a half to two times over the year. This was accompanied by qualitative growth: the level of service increased, the appearance and interior of stores changed, the assortment expanded, new sales technologies were introduced. In the process of changing shoe retail formats, a culture of consumption of branded shoes was formed, the clientele flowed to branded stores aimed at customers loyal to certain brands. This trend contributed to a decrease in the share of markets in the structure of the main places for buying shoes.

Another interesting feature of the Russian shoe market is the growing popularity of multi-brand stores.

Over the past two years, Russian retail players have been increasing the number of stores, wishing to “stake out” as many profitable trading floors as possible. Retail chains feared the arrival of international companies on the Russian market. However, the crisis has made its own adjustments. Western players never appeared. For example, in our market there are no such leading world chains as Deichmann (Germany, 2324 shoe stores in 17 countries, of which 1107 are in Germany); American network Famous Footwear (1100 stores); American company Genesco Inc (2000 retail stores of footwear and hats in the USA, Puerto Rico and Canada; shoe chains: Journeys, Journeys Kidz, Shi by Journeys, Underground Station, Johnston & Murphy, Lids, Lids Kids). The only exception is BATA, which is trying to win a domestic buyer for the fourth time. There are several reasons why there are only domestic multi-brand operators on the Russian market: a large amount of necessary investments (including in the product), high administrative barriers, as well as climatic features that require a special - winter assortment in the assortment, unusual for both Europe and America.

Response to the crisis and market development prospects

Objectively, the situation in which the shoe industry enterprises found themselves is not today. Russian retail companies still have neither understanding nor experience in building an assortment matrix. For this, sufficient organizational and financial resources and accumulated consumption statistics in a particular city are required. And to get it, you need a sufficient sample, sufficient experience and analysis of past sales with the right conclusions for the next season.

In addition, shoe retail operators must have the functional skills necessary for retail companies: logistics schemes, export operations, a management and accounting system, set management, and staff training. So far, shoe retail has something to work with.

The crisis was just a catalyst for the problems that were ripening: lack of competent management, over-ordering or overproduction of products due to optimistic planning, inadequate debt burden. At the same time, the unpredictability of the weather of the last four seasons has increased the demand dips in the off-season.

In a crisis, there has been a tendency to abandon unprofitable retail stores as part of a cost-cutting strategy. Similar measures are taken by the networks: Mattino, Zenden. The strategy of focusing on core competency involves abandoning new projects and focusing efforts in a more profitable direction. This strategy is used by the companies Obuv Rossii, Rieker, Ralf Ringer.

The crisis hit hard on Russian operators who work on borrowed funds. Banks have changed not only interest rates, but also the requirements for collateral. Few banks today regard goods (shoes) as collateral. Most market participants do not own premises or own production.

The deterioration of the state will be facilitated by the decline in economic indicators in the country, which will entail an already marked decline in purchasing activity of the Russian population, including footwear consumption in certain segments.

However, according to FCG, in the 2009 year, the market size as a whole will not change. In the segment of women's shoes, a reduction of about 5% is possible; most likely, there will be no changes in the segment of men's shoes. Negatively effective sales of women's shoes will be affected by a decrease in solvent demand, as well as the transition of customers to cheap price segments.

Growth is most likely in the segment of children's shoes - about 15%. The optimistic factors affecting the purchase of shoes for children are: increased fertility; greater than in adult shoes, the frequency of purchases due to the increase in the size of the child and increased wear; children mostly buy high-quality, and therefore expensive shoes.

Upper price segments and the upper middle of the Better segment will suffer the most. Moreover, the shift in preferences will occur precisely in the direction of the Contemporary (Good) and Moderate segments. Of course, the demand for shoes in the Budget segment will increase, but this is short-term growth, which will end as soon as the peak crisis wave stops, as soon as the crisis goes into decline.

Most likely, consumer consciousness as a whole will again change to the pre-crisis one and a half to two years (for different social groups - from six months to three years), experts say.

# EXPERT #

Results of the round table of shoemakers with the Ministry of Industry and Trade of the Russian Federation, CRPT, NOBS and Wildberries

World Footwear Yearbook: Global footwear production reaches 23,9 billion pairs and is back to pre-pandemic levels

How to double the sales of a shoe store?

New direction of exhibitions in Alma-Ata: Euro Shoes @ Elite Line & CAF

Round table with representatives of shoe factories of Dagestan with the support of the Ministry of Industry and Trade and NOBS

Coach turned to Big Data analysis and won the interest of a young audience

American handbag brand Coach has planned the success of its Tabby model among a younger audience, Generation Z, by turning to big data analysis, abandoning traditional and analogue tools, such as human intuition or the ability of any executive to sense “which way the wind will blow,” writes B.O.F.

Coach turned to Big Data analysis and won the interest of a young audience

American handbag brand Coach has planned the success of its Tabby model among a younger audience, Generation Z, by turning to big data analysis, abandoning traditional and analogue tools, such as human intuition or the ability of any executive to sense “which way the wind will blow,” writes B.O.F.

IDOL updates the concept

The IDOL brand, part of the Melon Fashion Group portfolio, opened the first flagship in an updated concept in the Aviapark shopping center in Moscow.

IDOL updates the concept

The IDOL brand, part of the Melon Fashion Group portfolio, opened the first flagship in an updated concept in the Aviapark shopping center in Moscow.

Louis Vuitton opens a new factory in Italy

Louis Vuitton has opened its second shoe factory in Italy. After opening the first one in Fiesso d'Artico in Veneto, the LVMH flagship brand has just opened a new production site dedicated to this category of footwear in the industrial zone of Civitano in the Marche region. There is also another brand production facility in Tuscany, where bags and leather accessories are produced, writes fr.fashionnetwork.com.

Louis Vuitton opens a new factory in Italy

Louis Vuitton has opened its second shoe factory in Italy. After opening the first one in Fiesso d'Artico in Veneto, the LVMH flagship brand has just opened a new production site dedicated to this category of footwear in the industrial zone of Civitano in the Marche region. There is also another brand production facility in Tuscany, where bags and leather accessories are produced, writes fr.fashionnetwork.com.

The Euro Shoes@CAF exhibition will be held in Almaty

From March 11 to 13, the Euro Shoes@CAF (Central Asia Fashion) exhibition will be held in Almaty at the Atakent exhibition complex. The exhibition, which is the largest international event in the fashion industry in Central Asia, will present collections of clothing, shoes and accessories.

The Euro Shoes@CAF exhibition will be held in Almaty

From March 11 to 13, the Euro Shoes@CAF (Central Asia Fashion) exhibition will be held in Almaty at the Atakent exhibition complex. The exhibition, which is the largest international event in the fashion industry in Central Asia, will present collections of clothing, shoes and accessories.

Euro Shoes will start operating on February 19 in Moscow!

The winter session of the international exhibition of footwear and accessories Euro Shoes premiere collection will be held in Moscow at the Expocenter from February 19 to 22. The organizers promise the presence of all the main participants at the exhibition, as well as new names from Europe, Asia and Russia.

Euro Shoes will start operating on February 19 in Moscow!

The winter session of the international exhibition of footwear and accessories Euro Shoes premiere collection will be held in Moscow at the Expocenter from February 19 to 22. The organizers promise the presence of all the main participants at the exhibition, as well as new names from Europe, Asia and Russia.

American buyers couldn't buy Birkin bags and sued Hermès

French fashion house Hermès is facing a lawsuit in California from two customers who were unable to purchase exclusive Birkin bags. The fashion house is accused of unfair commercial practices.

American buyers couldn't buy Birkin bags and sued Hermès

French fashion house Hermès is facing a lawsuit in California from two customers who were unable to purchase exclusive Birkin bags. The fashion house is accused of unfair commercial practices.

Why Rendez-Vous and Yandex Lavka released a “bread bag”

Shoe retailer Rendez-Vous announced the launch of a spring collaboration with Yandex Lavka and released a roll that resembles the shape of a woman’s handbag. This “Bread Bag” is presented in the Yandex.Lavka application at a price of 249 rubles. On the product packaging there is a promotional code for 1000 rubles, which can be spent in the Rendez-Vous network.

Why Rendez-Vous and Yandex Lavka released a “bread bag”

Shoe retailer Rendez-Vous announced the launch of a spring collaboration with Yandex Lavka and released a roll that resembles the shape of a woman’s handbag. This “Bread Bag” is presented in the Yandex.Lavka application at a price of 249 rubles. On the product packaging there is a promotional code for 1000 rubles, which can be spent in the Rendez-Vous network.

Camper has released innovative sneakers - designers

Spanish brand Camper's new Roku sneaker features six interchangeable components to create up to 64 different looks and color combinations. Roku means "six" in Japanese.

Camper has released innovative sneakers - designers

Spanish brand Camper's new Roku sneaker features six interchangeable components to create up to 64 different looks and color combinations. Roku means "six" in Japanese.

Christian Louboutin presented a collection in a cowboy style

At the Loubi Show in Paris, the French luxury brand Christian Louboutin presented its fall 2024 collection, following the trend - in the style of the Wild West. It included cowboy boots and rhinestone loafers.

Christian Louboutin presented a collection in a cowboy style

At the Loubi Show in Paris, the French luxury brand Christian Louboutin presented its fall 2024 collection, following the trend - in the style of the Wild West. It included cowboy boots and rhinestone loafers.

Fashion Week takes place in Moscow

Fashion Week takes place in the Russian capital. Events include fashion shows, markets where you can purchase clothes, bags and accessories, and a B2B Showroom for fashion industry professionals.

Fashion Week takes place in Moscow

Fashion Week takes place in the Russian capital. Events include fashion shows, markets where you can purchase clothes, bags and accessories, and a B2B Showroom for fashion industry professionals.

Turkish brand Vaneda on Euro Shoes

Street style, sport, outdoor, military – the main style directions of footwear of the company from Turkey

Turkish brand Vaneda on Euro Shoes

Street style, sport, outdoor, military – the main style directions of footwear of the company from Turkey

Kari accuses Zenden of unfair competition and is suing the FAS

The largest Russian shoe chain, Kari, appealed to the Moscow Arbitration Court to declare the actions of the Federal Antimonopoly Service (FAS) illegal, writes RBC.

Kari accuses Zenden of unfair competition and is suing the FAS

The largest Russian shoe chain, Kari, appealed to the Moscow Arbitration Court to declare the actions of the Federal Antimonopoly Service (FAS) illegal, writes RBC.

Fashion trends Fall-Winter 2023/24 for commercial footwear purchases

Permanent contributor to Shoes Report. Elena Vinogradova, an expert in sales and purchases in the fashion business, prepared an overview of the trends for the autumn-winter 2023/24 season especially for us.

Fashion trends Fall-Winter 2023/24 for commercial footwear purchases

Permanent contributor to Shoes Report. Elena Vinogradova, an expert in sales and purchases in the fashion business, prepared an overview of the trends for the autumn-winter 2023/24 season especially for us.

MSCHF and Crocs launch "Big Yellow Boots"

Creator of the Big Red Boots, Brooklyn brand MSCHF has teamed up with American plastic clog and sandal brand Crocs for another oversized shoe. The new Big Yellow Boots will go on sale on August 9th.

MSCHF and Crocs launch "Big Yellow Boots"

Creator of the Big Red Boots, Brooklyn brand MSCHF has teamed up with American plastic clog and sandal brand Crocs for another oversized shoe. The new Big Yellow Boots will go on sale on August 9th.

Five rules of professional lighting for a shoe store - something that is relevant in any season

When developing a lighting concept for shoe retailers, it is important to take into account not only the history of the brand, the architectural content of the premises, the target audience of the stores, but also the seasonality of the goods. With the onset of the cold season, client preferences change: bright weightless shoes are replaced by more massive models in discreet dark colors. Despite significant differences in summer and winter collections, the overall philosophy of the brand, its recognition should remain unchanged at any time of the year. Tatyana Ryzhova, an SR lighting expert in fashion retail, has identified five basic rules for a competent lighting concept for a shoe store for readers of the magazine, which will help to present winter assortment to customers in a winning way.

Five rules of professional lighting for a shoe store - something that is relevant in any season

When developing a lighting concept for shoe retailers, it is important to take into account not only the history of the brand, the architectural content of the premises, the target audience of the stores, but also the seasonality of the goods. With the onset of the cold season, client preferences change: bright weightless shoes are replaced by more massive models in discreet dark colors. Despite significant differences in summer and winter collections, the overall philosophy of the brand, its recognition should remain unchanged at any time of the year. Tatyana Ryzhova, an SR lighting expert in fashion retail, has identified five basic rules for a competent lighting concept for a shoe store for readers of the magazine, which will help to present winter assortment to customers in a winning way.

Bertsy: what to look for when choosing a model

Bertsy and tactical boots are becoming more and more relevant footwear, and not only because of the start of the hunting season. In Russia, there are several dozen enterprises producing this type of footwear. Oleg Tereshin, Deputy Chief Technologist of ZENDEN, told Shoes Report about the differences and features of ankle boots and what you should pay attention to when buying them in specialized retail and online.

Bertsy: what to look for when choosing a model

Bertsy and tactical boots are becoming more and more relevant footwear, and not only because of the start of the hunting season. In Russia, there are several dozen enterprises producing this type of footwear. Oleg Tereshin, Deputy Chief Technologist of ZENDEN, told Shoes Report about the differences and features of ankle boots and what you should pay attention to when buying them in specialized retail and online.

I doubt and object: how to find an approach to difficult clients?

How good and serene would be the work of a salesperson if the customers were calm, cheerful, always knew exactly what they wanted, and bought, bought, bought! It is a pity that this is possible only in dreams. Therefore, we will not dream, but we will act. Together with Maria Gerasimenko, a permanent author of SR, we understand the doubts and objections of buyers and build a strategy for working with them. Our expert pays special attention to the two main objections of buyers, on which 82% of sales are lost.

I doubt and object: how to find an approach to difficult clients?

How good and serene would be the work of a salesperson if the customers were calm, cheerful, always knew exactly what they wanted, and bought, bought, bought! It is a pity that this is possible only in dreams. Therefore, we will not dream, but we will act. Together with Maria Gerasimenko, a permanent author of SR, we understand the doubts and objections of buyers and build a strategy for working with them. Our expert pays special attention to the two main objections of buyers, on which 82% of sales are lost.

EURO SHOES presents an updated section of the GLOBAL SHOES exhibition with collections of shoe and bag brands from Asian countries

EURO SHOES premiere collection is expanding. Along with the traditional pool of leading European footwear brands from Germany, Spain, Italy and Turkey, several dozen footwear and bag brands from the Middle Kingdom will be presented in the GLOBAL SHOES section at the Moscow Expocentre from August 29 to September 1.

EURO SHOES presents an updated section of the GLOBAL SHOES exhibition with collections of shoe and bag brands from Asian countries

EURO SHOES premiere collection is expanding. Along with the traditional pool of leading European footwear brands from Germany, Spain, Italy and Turkey, several dozen footwear and bag brands from the Middle Kingdom will be presented in the GLOBAL SHOES section at the Moscow Expocentre from August 29 to September 1.

World Footwear Yearbook: Global footwear production reaches 23,9 billion pairs and is back to pre-pandemic levels

The Portuguese association of shoe manufacturers APICCAPS published the 13th edition of the international statistical bulletin World Footwear Yearbook for 2023, according to which in 2022 the production and export of shoes worldwide increased by 7,6% and 9%, respectively, and the world production of shoes reached 23,9 billion couples and returned to pre-pandemic levels.

World Footwear Yearbook: Global footwear production reaches 23,9 billion pairs and is back to pre-pandemic levels

The Portuguese association of shoe manufacturers APICCAPS published the 13th edition of the international statistical bulletin World Footwear Yearbook for 2023, according to which in 2022 the production and export of shoes worldwide increased by 7,6% and 9%, respectively, and the world production of shoes reached 23,9 billion couples and returned to pre-pandemic levels.

Rostov footwear brand Novak presented a collection of sneakers and sneakers

In the spring-summer 2023 season, the Rostov-on-Don shoe brand Novak presented a cute collection of sneakers and sneakers for every day. The upper of the shoe is made of genuine leather, suede, nubuck, the sole is made of light EVA.

Rostov footwear brand Novak presented a collection of sneakers and sneakers

In the spring-summer 2023 season, the Rostov-on-Don shoe brand Novak presented a cute collection of sneakers and sneakers for every day. The upper of the shoe is made of genuine leather, suede, nubuck, the sole is made of light EVA.

Jacquemus x Nike collaboration released

The second collaboration between Jacquemus and Nike, which has been talked about so much, is finally out. The appearance of the couple for many was a surprise. The model of Nike Air Force 1 sneakers, which was taken as the basis of the new collection, has undergone significant changes.

Jacquemus x Nike collaboration released

The second collaboration between Jacquemus and Nike, which has been talked about so much, is finally out. The appearance of the couple for many was a surprise. The model of Nike Air Force 1 sneakers, which was taken as the basis of the new collection, has undergone significant changes.

Crocs releases a collaboration with Barbie

If Barbie ditched heels and wore crocs, they would be pink. It was this collection in pink that was released by the American brand of plastic clogs Crocs, for the release of the film "Barbie" in the United States.

Crocs releases a collaboration with Barbie

If Barbie ditched heels and wore crocs, they would be pink. It was this collection in pink that was released by the American brand of plastic clogs Crocs, for the release of the film "Barbie" in the United States.

Shoe educational program: what shoe soles are made of

“What is the difference between TEP and EVA? What does tunit promise me? Is PVC glue? What is the sole of these shoes made of? ”- the modern buyer wants to know everything. In order not to smash his face in front of him and be able to explain whether such a sole suits him in soles, carefully read this article. In it, process engineer Igor Okorokov tells what materials the soles of shoes are made of and what makes each of them so good.

Shoe educational program: what shoe soles are made of

“What is the difference between TEP and EVA? What does tunit promise me? Is PVC glue? What is the sole of these shoes made of? ”- the modern buyer wants to know everything. In order not to smash his face in front of him and be able to explain whether such a sole suits him in soles, carefully read this article. In it, process engineer Igor Okorokov tells what materials the soles of shoes are made of and what makes each of them so good.

How to set prices that will earn

Some businessmen still confuse the concept of margin with the concept of trade margins and set prices for their goods, guided solely by the example of competitors. No wonder they go broke! Analyst at the Academy of Retail Technologies Maxim Gorshkov gives several tips and formulas with which you can set not only ruinous, but also profitable prices.

How to set prices that will earn

Some businessmen still confuse the concept of margin with the concept of trade margins and set prices for their goods, guided solely by the example of competitors. No wonder they go broke! Analyst at the Academy of Retail Technologies Maxim Gorshkov gives several tips and formulas with which you can set not only ruinous, but also profitable prices.

Sales of shoes and accessories: effective techniques for business rhetoric

Which speech modules are effective in communicating with potential and current customers of shoe stores, and which are not, Anna Bocharova, a business consultant, knows.

Sales of shoes and accessories: effective techniques for business rhetoric

Which speech modules are effective in communicating with potential and current customers of shoe stores, and which are not, Anna Bocharova, a business consultant, knows.

We form the salary of sellers: expert advice

“How do you charge your consultants for personal or general sales?” Is one of the most popular questions causing a lot of controversy and gossip on the online forums of retail business owners. Indeed, how to properly form the earnings of sellers? But what about bonuses, where to get a sales plan from, do employees allow them to buy goods at discounted stores? In search of truth, the Shoes Report turned to a dozen shoe retailers, but no company wanted to disclose its motivation system - the process of its development was too complicated and individual. Then we asked four business consultants, and finally became convinced that the topic of seller motivation is very complex, because even our experts could not come to a common opinion.

We form the salary of sellers: expert advice

“How do you charge your consultants for personal or general sales?” Is one of the most popular questions causing a lot of controversy and gossip on the online forums of retail business owners. Indeed, how to properly form the earnings of sellers? But what about bonuses, where to get a sales plan from, do employees allow them to buy goods at discounted stores? In search of truth, the Shoes Report turned to a dozen shoe retailers, but no company wanted to disclose its motivation system - the process of its development was too complicated and individual. Then we asked four business consultants, and finally became convinced that the topic of seller motivation is very complex, because even our experts could not come to a common opinion.

Technology Selling Issues

There is nothing worse than meeting the buyer with the words “Hello, can I help you with something?”, Because the seller works in the store just to help. Criticizing this well-established pattern of communication with the buyer, Andrei Chirkarev, business coach for effective sales and the founder of the New Economy project, shares the technology of truly selling issues with readers of Shoes Report.

Technology Selling Issues

There is nothing worse than meeting the buyer with the words “Hello, can I help you with something?”, Because the seller works in the store just to help. Criticizing this well-established pattern of communication with the buyer, Andrei Chirkarev, business coach for effective sales and the founder of the New Economy project, shares the technology of truly selling issues with readers of Shoes Report.

The whole truth about Bayer. Who is he and how to become one?

Bayer is no longer a new, but still a popular and sought-after profession. It’s fashionable to be a buyer. Buyers are at the origins of the emergence and development of trends. If the designer offers his vision of fashion in the season, then the buyer selects the most interesting commercial ideas. It is on buyers that the policy of sales of stores and what, in the end, the buyer will wear depends on. This profession is surrounded by a magical fleur, often associated with a lack of understanding of what exactly is the work of a buyer.

The whole truth about Bayer. Who is he and how to become one?

Bayer is no longer a new, but still a popular and sought-after profession. It’s fashionable to be a buyer. Buyers are at the origins of the emergence and development of trends. If the designer offers his vision of fashion in the season, then the buyer selects the most interesting commercial ideas. It is on buyers that the policy of sales of stores and what, in the end, the buyer will wear depends on. This profession is surrounded by a magical fleur, often associated with a lack of understanding of what exactly is the work of a buyer.

Fur, and not only: types of lining

In the production of winter footwear, various materials are used that are designed to retain heat and meet the requirements of consumers: natural sheepleather, artificial fur, artificial fur from natural wool and others. All types of lining fur have their own advantages and disadvantages. Let's consider the properties of each of them.

Fur, and not only: types of lining

In the production of winter footwear, various materials are used that are designed to retain heat and meet the requirements of consumers: natural sheepleather, artificial fur, artificial fur from natural wool and others. All types of lining fur have their own advantages and disadvantages. Let's consider the properties of each of them.

The best models of Czech shoes of the past

In Soviet times, for shoes from Czechoslovakia sold under the Cebo brand, customers stood in line for four hours and did not regret it, because Czech shoes were considered to be of high quality, comfortable and fashionable. Shoe designer Juraj Shushka shared a photo archive of his collection with Shoes Report magazine, which contains the most interesting Cebo models from the 1940's to the 1980's.

The best models of Czech shoes of the past

In Soviet times, for shoes from Czechoslovakia sold under the Cebo brand, customers stood in line for four hours and did not regret it, because Czech shoes were considered to be of high quality, comfortable and fashionable. Shoe designer Juraj Shushka shared a photo archive of his collection with Shoes Report magazine, which contains the most interesting Cebo models from the 1940's to the 1980's.

Retail Arithmetic

Before you begin to solve specific problems, you need to find out how accurately all the leaders of your company understand the basic terminology of retail.

Retail Arithmetic

Before you begin to solve specific problems, you need to find out how accurately all the leaders of your company understand the basic terminology of retail.

How to fire a worker without tears, scandal and trial

Sooner or later, any manager is faced with the need to part with an employee. Properly and on time the dismissal procedure will save the company money, and the boss himself - nerves and time. But why sometimes, knowing that a break in relations is inevitable, we put off the decision for months?

How to fire a worker without tears, scandal and trial

Sooner or later, any manager is faced with the need to part with an employee. Properly and on time the dismissal procedure will save the company money, and the boss himself - nerves and time. But why sometimes, knowing that a break in relations is inevitable, we put off the decision for months?